Managing a [huge] family...

Can the RBI manage it all? ~a simplified analysis

“It ain’t a child’s play” - replied Mr. Ravi to his son, who was curious to learn what all it takes to manage a family. Well, ask your parents, Mr. Ravi isn’t wrong. Managing a family, especially the finances, isn’t so easy peasy. Now multiply this responsibility with a million times complexity and difficulty, and still you can’t imagine the stress plaguing the central banks; especially in times of crisis, as is now.

Consider our very own central bank, the Reserve Bank of India (RBI). It is in charge of the Monetary Policy of India. It’s like we have told it, “Dear RBI, you’re the supremo of India’s financial and economic environment. You’ve got to ensure that we have an optimal growth. But hey, that doesn’t mean prices should touch the sky, no. You have to see that too. And all of this not at the cost of a volatile rupee. Also, please look after our banks. Be our superhero in times of need. We don’t know how you’ll do all of this, but you have to. It’s on you, sorry.”

Naturally, there are huge challenges in front of the RBI. Cause the gravity of one wrong decision could jeopardize the situation of the whole nation. And it’s incumbent on us to talk about this…

(As you continue reading this piece, I request you to go slow, as it will enable you to relate stuff and capture the bigger picture.)

The Growth-Inflation Dilemma

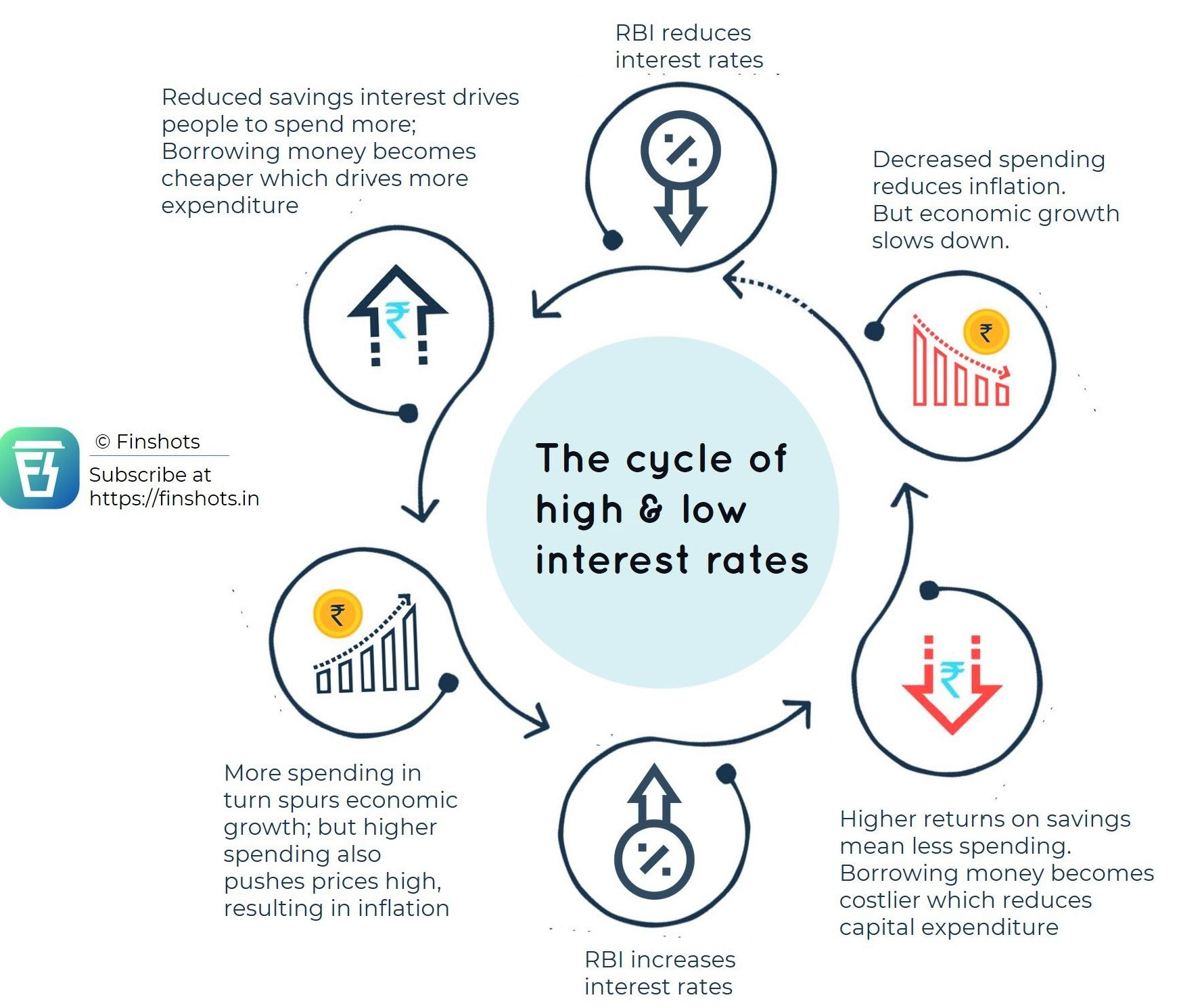

Take your time and study this inforgaph from the Finshots.in –

Both economic growth and inflation are positively correlated. You reduce the interest rates, and both of them move up, and vice-versa. Interest rate is akin to a ‘double-edged sword’. A single tactic could either help you or hurt you. Thus, the RBI’s dilemma is how to strike a perfect balance between economic growth and optimal inflation. Nonetheless, such a ‘divine coincidence’ is rare!

Consider India. Let’s rewind… pandemic broke out. Nation was locked-down. People weren’t spending. Lackluster demand. Economic growth was halted. The onus was on the RBI to help us recover from this shock. It had to make people to go and spend. So, it reduced the interest rates successively to 4%, so that people have no incentive to store money in banks, they can borrow at cheaper rates, and thus, they will spend. Besides, the Government was in dire need of funds. So, the RBI funded Government debt. Open Market Operations (OMO) were conducted which added more liquidity to the market; i.e. the RBI purchased (financed) Government bonds (debt) and thus paid money in return, which increased the supply of money in the market. Although it has also been selling bonds, the net effect was that purchases were quite higher. In fact, till 31st July, ₹1,24,154 Crores was injected to the market through OMOs. Other targeted liquidity injection programs were also conducted like T-LTRO. All of this contributed to the liquidity in the system and it seemed demand will be back to normal any time soon. This liquidity also empowered the ‘pseudo-healthy’ stock markets. Cash liquidity was high in the markets but credit growth was slow (~ 6.6% after considering inflation) due to the fear of risk of lending among banks, lack of clarity of the moratorium, etc. Anyway, at one point, we even reached a liquidity overflow of ₹8 Trillion. If you aren’t imagining, you should note that this is huge! Well, how did we mess it up then?

See, we can’t say all of this was vulnerable, but the fact that supply chains were affected the worst (due to lockdown) boomeranged the entire game! Forget balancing growth and inflation, in fact we messed up both of them. While the economic growth turned negative, the interest rate reductions and liquidity measures increased the supply of money in the market, which in turn, pushed inflation beyond the target range of RBI! Remember the ‘double-edged sword’ we talked about? Yes yes that one.. that stabbed us twice! Pretty harsh, it was!

{A primer — if you aren’t aware how India has messed up in various aspects, I recommend you to read our previous articles on GDP, Inflation and Forex. Anyway for a recap — negative growth rate of ~24% (the worst), inflation rate for august at 6.69% (consistently above RBI’s target range) and value of rupee depreciating! And now, join me as we talk about a bigger conundrum than the growth-inflation dilemma! Yes, you heard it right, it’s a trilemma - The Impossible Trilemma}

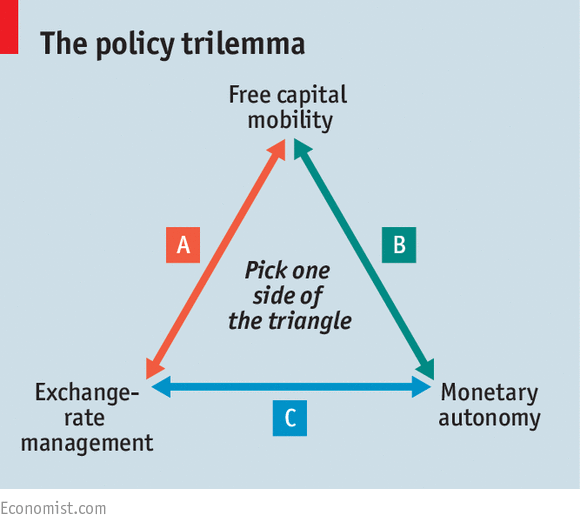

The Impossible Trilemma

Now, enter the international market. See, we’re an open economy – we conduct imports and exports, we allow foreign investors to come and invest in our country. And we haven’t kept our currency fixed; i.e. we’ve chosen to allow market forces (demand and supply) to decide the value of rupee. Now when you integrate domestic monetary policy (that we discussed above) with this open economic environment, it gives a way for conflicting objectives. How, you ask? Well, allow me to explain it in the context of India.

India is one of the emerging economies. Foreign investors are always in a treasure hunt to invest in such economies with a strong growth potential. And as the pandemic struck, assets (shares and bonds) in India fell down to dirt-cheap prices. This lured the foreign investors in, to come and invest in the under-valued Indian market. Capital inflows started pouring in (think of the humongous foreign investments in Jio). Between April and August alone, the foreign investment in India was $27 Billions! To invest in India, foreigners had to purchase our currency (rupee). As they purchased rupees, its demand increased and this led to an appreciation in the value of rupee (when demand > supply, price increases). But appreciation in the value of rupee makes it more expensive for foreigners and thus, it badly impacts our (already affected) exports. So, this had to be controlled. To do that, the RBI had to sell rupee and purchase dollars. And it did. In fact, by virtue of our dollar purchases (accumulation), our foreign exchange reserves touched an all-time high of $540 Billions!

Now think about this - as the RBI buys dollars and sells rupees, it increases the supply of money (read: rupees) in the market. Excessive money in the market could prompt people to over-spend, and this could lead to inflation! To avoid this, ideally, the RBI should have tried to squeeze out liquidity from the system. How, you ask? Well, by increasing the interest rates (as it makes borrowing expensive and deposits lucrative, thus, people spend less) or by selling Government bonds (if RBI sells, people buy, and thus money is extracted from the market). But wait… squeezing money out of the market could have slowed down the growth even more (as people will spend less)! And that is where the conflict arises, my friend!

Economic growth and capital inflows were given higher priority over inflation control. Thus, the RBI had to keep adding more and more liquidity to the market by cutting the interest rates and other liquidity measures (we previously talked about). This further supply of money in the market and a disruption of supply chains created a gap in the demand-supply dynamics. Against what was planned, the demand didn’t improve significantly! To add to our agony, supply shocks emerged! And now you know what led us to the present situation of high inflation in spite of negative growth and excessive capital inflows!

That’s it — a live example of the principle of Impossible Trinity (or Trilemma). The Impossible Trilemma states that a country may not be able to stabilise the exchange rate, and conduct an independent monetary policy when it is financially integrated with the rest of the world.

Basically, out of this triangle, you can choose to have any one side; i.e. you can control any two of the three vertices and not all three (domestic monetary policy, stable rupee, capital inflows). Think of three naughty children, you somehow manage two of them, but one must be set free!

Anyway, as The Economist points out –

“Three out of three ain’t possible, but two out of three ain’t bad.”

Which side of the triangle?

“Every choice is a renunciation. Indeed. Every choice is a thousand renunciations. To choose one thing is to turn one's back on many others.” - Ronald Rolheiser

Ever since the pandemic began, it’s been a headache for the central banks to choose an appropriate side of the triangle (we just saw) so that the respective country sails through smoothly. RBI is no exception. But while other central banks prioritized their objectives, our RBI thought of doing it the ‘Indian way’; i.e. to pursue all of them, rather aggressively. But, as we discussed, it’s proven to be counter-productive!

As Rajeswari Sengupta puts it succinctly —

[…] But if the RBI continues to ignore the Impossible Trilemma, it will eventually fail. There are two main ways this could happen: It might need to give up on its exchange rate objective, as the recently released report hints. Or it might need to give up on its inflation objective.

Both would be problematic. Exchange rate appreciation will further damage the already hard-hit export sector. But allowing high inflation is even more of a problem in a country where the RBI has committed to the public not to allow a repeat of what happened after the last global financial crisis, when inflation soared to double digits.

But can we blame it all on the RBI? Perhaps not. Because these measures could have been productive, had there been no inflation.

Anyway, as the credit growth is slow now, the perils aren’t quite visible. But once it picks up, the RBI will be forced to squeeze all this money from the market! Some economists opine that, perhaps, it might opt for other macro-prudential instruments like altering the Cash Reserve Ratio (CRR) or the Loan-To-Value ratio (LTV) to control the credit pick-up when it gains momentum in the future. Increasing the CRR (portion of deposits that can’t be given as loan by banks) or reducing the LTV (ratio of loan provided to the asset purchased) can help control the credit growth.

Also, when prices are rocketing high, a further interest rate reduction seems foolhardy. To cut a long story short, challenges before the RBI are rising. But the RBI will surely find a leeway amidst all the obstacles. But that has to be done with a proper planning and extreme caution.

And as HSBC’s Pranjul Bhandari puts it —

All told, while we believe the RBI will just about manage the situation by striking a balance across its various objectives, it will have to be vigilant, looking out for turning points.

The biggest challenge will perhaps come later when pandemic fears recede, activity picks back up, and central banks begin to withdraw liquidity globally. The RBI will have to move quickly then, withdrawing excess liquidity so it does not become inflationary, and yet do it without hurting the recovery. That debt maneuvering will perhaps be the RBI’s toughest challenge of all. But that is a problem for another day.

And all we can do is hope for the best! Our superhero will surely strike a note.

*touchwood*

Hey fellas, hope you found this article very intriguing! Honestly speaking, this is my personal favourite among all the articles in this blog. :)

But I must tell you, please don’t limit yourself to this article. Wherever required, I have provided links to some resourceful content (in ‘blue’ highlights) and in the ‘Further reading’ section below. If you need further clarification, take a step ahead, go there, study that article and quench your thirst. I believe that if I can make readers think of a topic in their perspective, only then, I can achieve my very basic objective of helping people make informed decisions.

So, thank you guys. If you have friends or family members who listen/read these news surrounding RBI, interest rate cuts, etc, but aren’t able to make a sense of it, please recommend this article to them. I can assure you this will give them a fairly clear idea of these stuff! So yeah, share it with your connections.

As always, I really appreciate all of your valuable feedback and suggestions. If you want to share something, feel free to revert back to me.

And yeah, if you think that this blog is consistent in terms of its content and other deliverable, please help us reach more and more readers.

By the way, if you haven’t already, please subscribe to the blog and never miss an update!

Thank you so much, all of you!

See you, take care, bye…

Happy Reading :)

Further reading:

RBI’s Third Eye by Pranjul Bhandari (highly recommended)

India’s Impossible Trilemma by Kotak Securities (for a layman)

Signing off,

Abhishek Sahoo